In Professor Plesner’s article, ‘There in no Real Estate Price Bubble’, The real issue of whether the prices of real estate in Israel today are based on a stable market or not, is poignantly raised and answered. I found this article to be very informative. Plesner dissects the topic in an objective and most scientific manner. Below is a translation of that article in English. Enjoy!

In Professor Plesner’s article, ‘There in no Real Estate Price Bubble’, The real issue of whether the prices of real estate in Israel today are based on a stable market or not, is poignantly raised and answered. I found this article to be very informative. Plesner dissects the topic in an objective and most scientific manner. Below is a translation of that article in English. Enjoy!

There is no speculative building in Israel, the prices of rent are not unrelated to the price of the apartments and it is just as hard to purchase an apartment in 2013 as it used to be. The former deputy governor of the Bank of Israel proves that the prices of apartments are based on a solid economic foundation.

The matter of housing is still in the top headlines, and with reason. When people in their late twenties and even in their early thirties are living with their parents, there is a problem. However, there is a problem with the problem: the problem of identifying the nature of the first problem. We will deal with both of them here, and also discuss somewhat the connection between all this and the Bank of Israel.

What is a bubble?

Identifying the first problem can be summarized by asking the question if this is about a real excess in demand for housing or a real estate bubble.

What is a bubble? A bubble develops when people buy apartments with a speculative motive – with a hope that the prices of apartments will rise and then they will get a significant return on their investment. The expected rise in prices needs to be significant, since many of the buyers take out a mortgage in order to finance the purchase. The rise in prices (in conjunction with rent, which is not a given – since a bubble means that you won’t necessarily find a tenant) needs to cover the cost of the mortgage and a return that is more than you would expect to make in the securities market.

If you look just at the rise in apartment prices in the last four or five years, you can understand why many people hypothesize that this is a bubble. Since the first quarter of 2008 until the second quarter of 2013 the average price of an apartment rose by 59%; even the actual price, in other words the price deducted from the consumer price index, rose by 37%. We are therefore talking about an actual yearly return in the amount of 5.9% just from the rise in housing prices without taking into account rent. That is definitely a pretty return on an investment.

Is it possible that a return like this could be derived from a real demand for housing, and not – at least partially – from speculation? The answer, which may surprise some of the readers, is positive.

How do we know this? Well, in Israel, as opposed to the United States, the test is simply relative, since the vast majority of construction is apartment buildings. It is entirely possible that in the United States a contractor will take a gamble and build a few single family homes without knowing ahead of time if he will have buyers. However, in Israel it is a far fetched idea that a contractor would build a building with, say, 15 apartments, without some of them having guaranteed buyers. And even if it happens here and there, it definitely doesn’t happen in a magnitude that could affect the supply of apartments. For this reason, it is not feasible that the supply of apartments will increase so significantly without there being a real demand, for housing needs or speculation needs.

Therefore, you can rely on the association between rental prices and the cost of an apartment as a test of the bubble question. The reason is simple: the rental price is the price that represents the net demand for housing, without all speculation and supply of rental apartments. The significance of a bubble from the stand point of the demand and the supply of housing is that the supply of apartments is greater, but the prices are rising at rates that would expel from the housing market those who are there for housing alone and they would not be able to purchase these apartments at the speculation-caused inflation. On the other hand, those who purchased apartments for speculation purposes would be interested to rent them out. The deeper meaning is that the supply of rental apartments will increase which will cause a decrease in rent prices while the purchase prices on the apartments themselves will rise.

From this we can understand that if the rent prices increase in value at the same rate as the purchase prices, we can deduce that speculation doesn’t play a real role in the prices. Or, if there is a component like that, the demand for housing by means of rent would increase at the same rate as the supply of these same types of apartments.

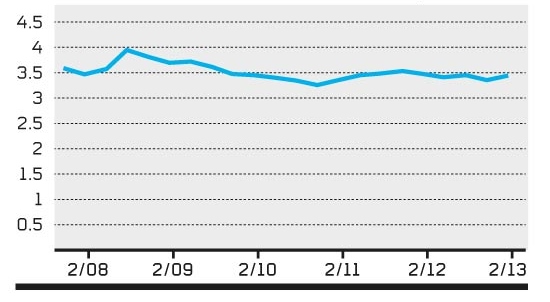

In a situation like this the concept of a “bubble” has no real meaning. Therefore, all that is necessary to be done is to examine what happened to the rental prices in comparison to the purchase prices. The examination is done by translating the rental prices in to terms of rate of return on the purchase price of the apartment (see table below). From the given information we can deduce that there was a very slight decreasing tendency in the rate of return from the forst quarter of 2008 until the second quarter of 2013.

However, it is necessary to add the fact that in January and February of 2008 the interest rate of the Bank of Israel was 4.25%. Which means that the rate of return on an apartment in the first quarter of 2008 – 3.6% approximately – was not a real great bargain. On the other hand, the interest rate of the Bank of Israel in second quarter of 2013 fluctuated between 1.75% in March and 1.25% in June. In these conditions, a return of 3.45% on the purchase price of an apartment is already looking more attractive. Additionally, the slight drop in the rate of return in the chart all but stopped in the forst quarter of 2011 and afterwards it seems to have had a slight rise. The conclusion here is clear: there is no trace of a bubble in the real estate prices in Israel.

The “low” of 1977

As it was stated, there is no bubble, but that is not enough to comfort those standing at the beginning of their road in front of the purchase prices of apartments that are so far from them as Moses was from the Land of Israel.

First a little history: The available income of an individual is the same income that he is entirely free to do with as he pleases. He has already paid his taxes and has received his transfer payments, so he has no partners in this income.

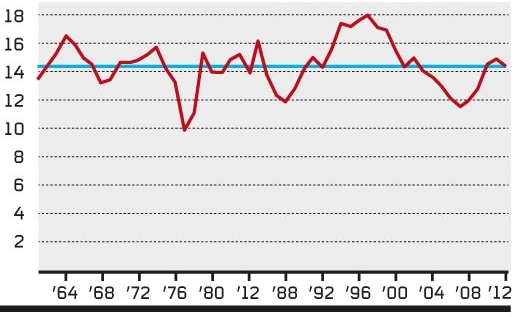

What is the number of years of available income per average person in Israel necessary in order to purchase an average apartment? The numbers are surprising (see chart below). The first number points to the fact that purchasing an apartment in Israel has always been a mission almost impossible. The second number points to the fact that the situation in the last few years is not so bad.

First of all, just to make it clear how forlorn and grave the situation is here, suffice it to say that in the United States in the last three years it was necessary to have 7.5 years of available income in order to purchase an average house; in Australia that number varied over the last 20 years between 7 and 9 years. And, yet, here in Israel, the long-term average is 14.5 years.

In order to illustrate the constant severity of the situation here, lets assume a household with two adults, and as such the available income of the household is double of that of an individual. Let’s assume that our average couple wants to buy an average apartment, whose price in relation to the available income is average according to the chart.

Compared with the income of the couple, the price of the apartment is therefore, 7 years and 3 months. The accepted notion is that you should not dedicate more than 25% of your available income for housing expenses. The intention here is that if said couple would dedicate the most that is possible to dedicate in order to finance housing, they would need 29 years in order purchase an apartment. And if, g-d forbid, they had the bad luck to be entering the housing market in 1995, for example, it would have taken them 34 and a half years in order to complete the purchase (this is all calculated before interest payments on the mortgage were taken in to consideration).

As for the question of what caused this situation, we will get to in a bit. In the meantime let’s turn to the second surprising finding: in the long term perspective, the situation today isn’t so bad.

What caused the feeling of housing prices being so expensive in the last few years is the fact that the price of housing in terms of income has increased since 2007. However this increase started from an all time low in 1977. And the reason for that low, by the way, is because the country built tens of thousands of housing units without buyers, an act which stemmed from the fears of politicians of the possibility that Israel would enter in to a recession after the Yom Kippur war as it did before the Six day war.

The monopoly and bureaucracy against the powers of the market

If it is so good, why, then, is it so bad? Two reasons for the situation: The first is the Israel Land Authority (formerly known as the Israel Land Administration). The national owner is a blow like no other in that it does not allow the supply of land to respond to the status of the market. The supply of land is determined by bureaucracy and not by the signals sent by the market.

What makes matters worse is that the Authority is in a major conflict of interests seeing as it constitutes a source of income for the treasury. It is even defined in the budget books as a body of business. Therefore, it has a great incentive to act as a monopoly, but being that it is a statutory body it is exempt from the regulation of the supervisor of business limitations.

The second reason is the intolerable bureaucracy of the bodies responsible for planning – the Planning Administration within the Ministry of Interior, the district and local committees. The planning process, therefore, takes years – at times even absurd amounts of time – and that’s why even when there is a “thawing” of land for building, you shouldn’t hold your breath for the building to actual start.

Finally, there is no serious building for rentals in Israel, despite all the efforts in the last few years (the last one, of course, was the Minister of Treasury Yair Lapid that even started a new governmental company to further the establishment of tens of thousands of apartments in rental projects). The guilty party is the “tenant protection” law from the time of the British mandate and the beginning years of the State of Israel. This law has totally destroyed building for rental, because in essence it is confiscating the property of the owner of the apartment in favor of the tenant. This is not unique to Israel: in any place where this law exists, the building for rental has been destroyed and has never returned even after the law was nullified.

He reason for this is clear: investing in housing is a very long term investment. Therefore, anything that heightens the uncertainty involved scares off the investor. And the discouragement is especially long term if the cause of the uncertainty is the government. This is because it is much harder to predict what a government will do than what the “powers of the market” will do.

The bottom line, no doubt, is: the housing problem is completely the handiwork of the governments of Israel throughout the years.

*The author is a Professor for Agricultural and Administrative Economics in Hebrew University and formerly the Deputy Governor if the Bank of Israel

Average apartment price in terms of years of available income on average per person

Average rent price in terms of rate of return on average apartment purchase price Percent per year, by quarter